取得するのは「Honeymoon Well Nickel Project」などのニッケル鉱山。すでにBHPが50%を出資するニッケル鉱山開発のJV(共同企業体)の残りの株式もノリリスクの子会社であるMPIニッケルから買い取る。

BHP has agreed to acquire the

Honeymoon Well Nickel Project comprising the

Honeymoon Well development project and a 50

per cent interest in the Albion Downs North and Jericho exploration

joint ventures from MPI Nickel Pty Ltd, a wholly owned subsidiary

of Norilsk Nickel Australian Holdings BV.

BHP Nickel West is

currently a 50 per cent shareholder in the Albion Downs North and

Jericho Joint Ventures.

BHP and Noront

Resources Ltd. today(2021/7/27) announced that they have entered into

a definitive Support Agreement pursuant to which BHP Western Mining

Resources International Pty Ltd , a wholly-owned subsidiary of BHP Lonsdale,

will make a take-over bid to acquire all of the issued

and outstanding common shares of Noront for C$0.55 per share in cash.

BHP Lonsdale owns 3.7% of the Noront shares on a fully diluted basis. The

total equity value of the transaction is C$325 million (based on 100% of the

fully diluted shares outstanding). The members of the Board of Directors of

Noront who voted on the matter unanimously recommend that Noront

shareholders tender their shares to accept the Offer.

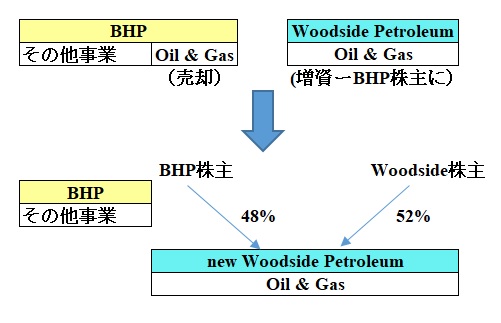

Woodside and BHP to create a global

energy company

Woodside Petroleum Ltd (“Woodside”) and

BHP Group (“BHP”) have entered into a merger commitment deed to combine

their respective oil and gas portfolios by an all-stock merger (the

“Transaction”) to create a global top 10 independent energy company by

production.

On completion

of the Transaction, BHP’s oil and gas business would merge with

Woodside, and Woodside would issue new shares to be distributed to BHP

shareholders. The expanded Woodside would be owned 52 per cent by

existing Woodside shareholders and 48 per cent by existing BHP

shareholders. The Transaction is subject to confirmatory due diligence,

negotiation and execution of full form transaction documents, and

satisfaction of conditions precedent including shareholder, regulatory

and other approvals.

With the combination of two high

quality asset portfolios, the proposed merger would create the largest

energy company listed on the ASX, with a global top 10 position in the

LNG industry by production. The combined company will have a high margin

oil portfolio, long life LNG assets and the financial resilience to help

supply the energy needed for global growth and development over the

energy transition.

Attractive strategic and

financial rationale

The combination of Woodside and BHP’s

oil and gas business is expected to deliver substantial value creation

for both sets of shareholders from across a range of areas, including:

Greater scale and diversity of

geographies, products and end markets through an attractive and

long-life conventional portfolio

Resilient, high margin operating

cash flows to fund shareholder returns and business evolution to

support the energy transition

Strong growth profile with a

plan to achieve targeted Scarborough FID in the 2021 calendar year

and capacity to phase the most competitive, high-return options

within the portfolio

Proven management and technical

capability from both companies

Shared values and focus on

sustainable operations, carbon management and ESG leadership

Estimated synergies of more than

US$400 million (100 per cent basis, pre-tax) per annum from

optimising corporate processes and systems, leveraging combined

capabilities and improving capital efficiency on future growth

projects and exploration

Greater financial resilience,

relative to Woodside’s and BHP’s standalone petroleum businesses.

Woodside CEO and Managing Director

Meg O’Neill said, “Merging Woodside with BHP’s oil and gas business

delivers a stronger balance sheet, increased cash flow and enduring

financial strength to fund planned developments in the near term and new

energy sources into the future.

“The proven capabilities of both

Woodside and BHP will deliver long-term value for shareholders through

our geographically diverse and balanced portfolio of tier 1 operating

assets and low-cost and low-carbon growth opportunities.

“The proposed transaction

de-risks and supports Scarborough FID later this year and enables more

flexible capital allocation. We will continue reducing carbon emissions

from the combined portfolio towards Woodside’s ambition to be net zero

by 2050.”

BHP CEO Mike Henry said, “The

merger of our petroleum assets with Woodside will create an organisation

with the scale, capability and expertise to meet global demand for key

oil and gas resources the world will need over the energy transition.

“Bringing the BHP and Woodside

assets together will provide choice for BHP shareholders, unlock

synergies in how these assets are managed and allow capital to be

deployed to the highest quality opportunities. The merger will also

enable the skills, talent and technology of both organisations to build

a resilient future as the world’s needs evolve.”

Greater scale and diversity of

geographies, products and end markets to create a long-life conventional

portfolio

This Transaction delivers significant

benefits for both Woodside and BHP shareholders by creating a long-life

conventional portfolio of scale and diversity of geography, product and

end markets.

On a proforma basis, the combined

business will consist of:

High quality conventional asset

base producing around 200 MMboe (FY21 net production)

Diversified production mix of

46% LNG, 29% oil and condensate and 25% domestic gas and liquids

(FY21 net production)

Wide geographic reach with

production from Western Australia, east coast Australia, US Gulf of

Mexico, and Trinidad and Tobago with approximately 94% of production

(FY21 net production) from OECD nations

2P reserves of over 2 billion

boe comprising 59% gas, and 41% liquids.

Resilient operating cash flows

to fund shareholder returns and business evolution to support the energy

transition

Significant operating cash flow will

support continued strong returns to shareholders over time. Woodside

will maintain its focus on disciplined growth investment and continued

dividends. It is expected that Australian shareholders will benefit from

the distribution of Woodside’s significant franking credit balance.

Strong growth profile with a

plan to achieve targeted Scarborough FID in 2021 and capacity to phase

high-return options

The Transaction will deliver expanded

growth optionality for shareholders with the flexibility to phase and

selectively progress near and longer term high-return options.

Woodside and BHP have developed a

plan to targeted final investment decision (FID) for Scarborough

(Australia) by the end of the 2021 calendar year, prior to the proposed

completion date for the merger.

As part of this plan, Woodside and

BHP have agreed an option for BHP to sell its 26.5 per cent interest in

the Scarborough Joint Venture to Woodside and its 50 per cent interest

in the Thebe and Jupiter joint ventures to Woodside if the Scarborough

Joint Venture takes a FID by 15 December 2021. The option is exercisable

by BHP in the second half of the 2022 calendar year and if exercised,

consideration of US$1 billion is payable to BHP with adjustment from an

effective date of 1 July 2021. An additional US$100 million is payable

contingent upon a future FID for a Thebe development.

The Atlantis Phase 3 (US), Mad Dog

Phase 2 (US), Shenzi North (US) and Sangomar Field Development Phase 1

(Senegal) projects remain on budget and on track, and along with

significant brownfield expansion options, provide opportunity for near-

and medium-term growth.

Longer term embedded options include

the Wildling (US), Trion (Mexico), Calypso (Trinidad and Tobago) and

Browse (Australia) projects. These options offer significant potential

growth coupled with multiple exploration opportunities and partnerships.

Proven management and technical

capability from both companies

The combined business will benefit

from the joint management and technical petroleum expertise of both

companies, led by Meg O’Neill as the CEO and Managing Director. Leading

HSE performance, LNG production and marketing, deepwater oil development

and production, exploration success, and international experience will

come together to create a differentiated set of capabilities. These

capabilities are further supplemented through investments in technology

and low carbon solutions, and strong governance systems. In addition, it

is intended that the Woodside Board will appoint a current BHP director

as a Woodside director on completion.

Shared values and focus on

sustainable operations, carbon management and ESG leadership

The combined business will continue

to have an unrelenting focus on safe, sustainable and reliable

operations, building on Woodside’s and BHP’s strong track records.

It will build on Woodside’s existing

targets to reduce net emissions by 15 per cent and 30 per cent by 2025

and 2030 respectively, on the pathway to its ambition of net zero by

2050, applying these to the combined portfolio. Progress will be

reported on both an operated and non-operated equity emissions basis.

In support of the goals of the Paris

Climate Agreement, and to contribute to the energy transition, the

combined business will focus on building and maintaining a high return

and carbon-resilient portfolio which includes natural gas and new energy

technologies.

The combined business is expected to

generate significant cash flow this decade to support the development of

new energy products and low carbon solutions including hydrogen, ammonia

and carbon capture and storage (CCS).

Synergies and benefits

This merger of highly complementary

asset portfolios is expected to unlock material synergies.

Woodside and BHP have estimated

annual synergies to be in excess of US$400 million per annum (100 per

cent basis, pre-tax).

These synergies are anticipated to

come from:

Optimising corporate processes

and operating costs across the entire portfolio

Leveraging the leading petroleum

capabilities of both organisations including technology, operating,

sales and marketing, infrastructure and resource development

expertise

Optimising spend on exploration

and future growth projects through the development of combined and

more capital efficient opportunities.

Greater financial resilience,

relative to Woodside and BHP’s standalone petroleum business

On completion of the Transaction, the

combined business’ balance sheet will be strengthened by the resilience

the merged portfolio delivers through the cycle. On a proforma basis (12

months to 30 June 2021), the combined business will have:

A large earnings base with

revenue of more than US$8 billion and EBITDA of US$4.7 billion

Operating cash flows of more

than US$3 billion supported by resilient foundation assets

A strong balance sheet reflected

with low gearing of 12%.

Merger mechanics

Under the proposed transaction,

Woodside, or a wholly owned subsidiary of Woodside, will acquire 100 per

cent of the issued share capital of BHP Petroleum International Pty Ltd

in exchange for shares in Woodside which will deliver 48 per cent to BHP

shareholders on completion. Woodside shares will be immediately

distributed to BHP shareholders. Woodside will remain listed on the ASX

with listings on additional exchanges being considered.

Both the Woodside and BHP boards of

directors confirm their support for the Transaction. The merger is

expected to be completed in the second quarter of the 2022 calendar year

with an effective date of 1 July 2021.

The Transaction is subject to

confirmatory due diligence, negotiation and execution of full form

transaction documents which is targeted for October 2021, and

satisfaction of conditions precedent including shareholder, regulatory

and other approvals. Under the merger commitment deed, each party has

agreed to pursue a merger transaction and agreed to certain exclusivity

arrangements and to each pay a reimbursement fee of approximately US$160

million in certain circumstances.

Woodside’s financial advisers are

Gresham Advisory Partners Limited and Morgan Stanley Australia Limited,

and its legal advisers are King & Wood Mallesons and Vinson & Elkins

LLP.

BHP’s financial advisers are J.P.

Morgan, Barclays and Goldman Sachs and its lead legal adviser is Herbert

Smith Freehills.

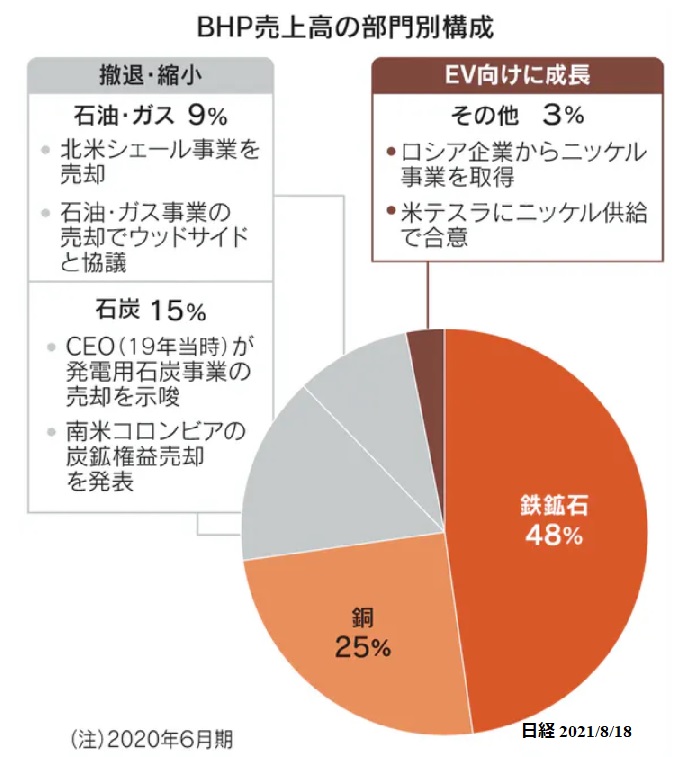

About BHP

BHP is the world’s largest

diversified natural resources company by market capitalisation with over

80,000 employees and contractors, primarily in Australia and the

Americas. BHP’s products are sold worldwide and it is among the world’s

top producers of major commodities, including iron ore, copper, nickel

and metallurgical coal.

BHP pioneered the development of an

oil and gas industry in Australia with the Bass Strait discovery in

1965. The BHP petroleum business now has conventional oil and gas assets

in the US Gulf of Mexico, Australia, Trinidad and Tobago, and Algeria,

and appraisal and exploration options in Mexico, Trinidad and Tobago,

western US Gulf of Mexico, Eastern Canada, and Barbados.

The crude oil and condensate, gas and

natural gas liquids (NGLs) produced by BHP’s petroleum assets are sold

on the international spot market or domestic market. The total gross

asset value of the BHP petroleum business as at 30 June 2021 was US$15.4

billion, it contributed US$3.9 billion to BHP group revenue and it

generated EBITDA of US$2.3 billion for the year ended 30 June 2021.

About Woodside

Woodside led the development of the

LNG industry in Australia and is applying this same pioneering spirit to

solving future energy challenges. With a focused portfolio, Woodside is

recognised for its world-class capabilities as an integrated upstream

supplier of energy. As Australia’s leading LNG operator, Woodside

operated 6% of global LNG supply in 2020. Woodside’s proven track record

and distinctive capabilities are underpinned by more than 65 years of

experience, making Woodside a partner of choice. Disclaimer and

important notice

Disclaimer and important notice

This announcement is subject to:

the same “Disclaimer, important

notice and assumptions” contained in pages 2 to 3 of Woodside’s

investor presentation titled “Woodside and BHP petroleum merger”

dated 17 August 2021; and

the same “Disclaimer” contained

in page 2 of BHP’s investor presentation titled “Growing value and

positioning for the future” dated 17 August 2021, each with any

necessary contextual changes.

ーーーーーーーーーーーーーーーーーーーーーーーーーーーー

BHP has today approved US$5.7 billion

(C$7.5 billion) in capital expenditure for the Jansen

Stage 1 (Jansen S1) potash project in the province of Saskatchewan, Canada.

BHP Chief Executive Officer, Mike Henry,

said Jansen is aligned with BHP’s strategy of growing our exposure to future

facing commodities in world class assets, which are large, low cost and

expandable.

“This is an important milestone for BHP

and an investment in a new commodity that we believe will create value for

shareholders for generations,” Mr Henry said. Jansen is located in the

world’s best potash basin and is expected to operate up to 100 years. Potash

provides BHP with increased leverage to key global mega-trends, including

rising population, changing diets, decarbonisation and improving

environmental stewardship.

“In addition to its merits as a

stand-alone project, Jansen also brings with it a series of high returning

growth options in an attractive investment jurisdiction. In developing the

Jansen project, BHP has had ongoing positive engagement and collaboration

with First Nations and local communities, and with the provincial and

federal governments. Jansen is designed with a focus on sustainability,

including being designed for low GHG emissions and low water consumption.”

Mr Henry added.

Jansen S1 is expected to produce

approximately 4.35 million tonnes of potash per annum

(footnote 1), and has a basin position with the potential for further

expansions (subject to studies and approvals). First ore is targeted in the

2027 calendar year, with construction expected to take approximately six

years, followed by a ramp up period of two years.

Jansen S1 includes the design,

engineering and construction of an underground potash mine and surface

infrastructure including a processing facility, a product storage building,

and a continuous automated rail loading system. Jansen S1 product will be

shipped to export markets through Westshore, in Delta, British Columbia and

the project includes funding for the required port infrastructure.

We anticipate that demand growth will

progressively absorb the excess capacity currently present in the industry,

with opportunity for new supply expected by the late 2020s or early 2030s.

That is broadly aligned with the expected timing of first production from

Jansen. Beyond the 2020s, the industry’s long run trend prices are expected

to be determined by Canadian greenfield solution mines. In addition to

consuming more energy and water than conventional mines like Jansen,

solution mines tend to have higher operating costs and higher sustaining

capital requirements.

At consensus prices (footnote 2), the

go-forward investment on Jansen is expected to generate an internal rate of

return of 12 to 14 per cent, an expected payback period of seven years from

first production and an underlying EBITDA margin of approximately 70 per

cent given its expected first quartile cost position.

We have previously acknowledged the

US$4.5 billion (pre-tax) of capital invested to date has resulted in a

significant initial outlay and that our approach would be different if

considering the project again today. The investment to date includes

construction of the shafts and associated infrastructure (US$2.97 billion

(footnote 3) scope of work), as well as engineering and procurement

activities, and preparation works related to Jansen S1 underground

infrastructure. The construction of two shafts and associated infrastructure

at the site is 93 per cent complete and expected to be completed in the 2022

calendar year. To date approximately 50 per cent of all engineering required

for Jansen S1 has been completed, significantly de-risking the project. If

the investment to date were to be included, the full cycle project would

yield a much lower internal rate of return.

As part of our 2021 financial results, we

have assessed the carrying value of the existing Potash asset base as at 30

June 2021 and have recognised a pre-tax impairment charge of US$1.3 billion

(US$2.1 billion after tax). The impairment charge against our Potash assets

reflects an analysis of recent market perspectives and the value that we

would now expect a market participant to attribute to our investments to

date.

Footnotes

1. The Jansen S1 project will convert

approximately 20% of the 5.23 billion tonnes Measured and Indicated Mineral

Resources into Ore Reserve (see Appendix 1).

2. Price assumptions reflect average of

CRU and Argus prices. Average 2027–2037: US$341/t CRU and US$292/t Argus.

IRR = Expected Jansen Stage 1 IRR across approximately 100 year mine life.

Jansen Stage 1 IRR is post[1]tax, nominal and reflects the range of the

average CRU and Argus prices, and excludes expenditure on shafts and

essential services consistent with previous disclosure.

3. The US$2.97 billion current scope of

work for Jansen is part of approximately US$4.5 billion that has been

invested on the project since 2008 ahead of the sanction decision on Jansen

Stage 1. Approximately US$220 million of the US$2.97 billion approved for

the current scope of work, expected to be completed in the 2022 calendar

year, is not yet spent. Sustaining capital for Jansen Stage 1 is expected to

be approximately US$15/t (real) long term average +/- 20% in any given year.

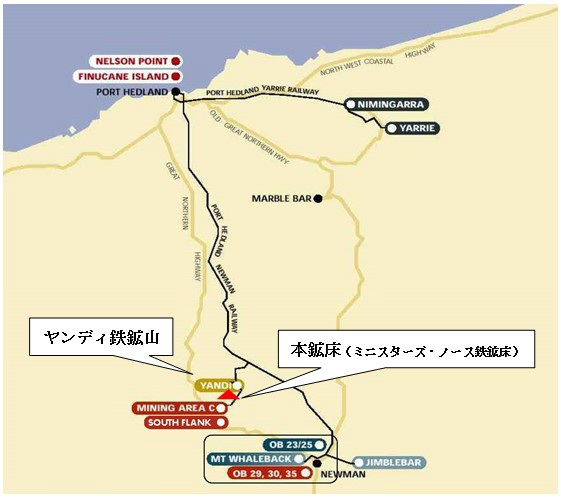

2025/9/18 伊藤忠と三井物産、西豪州ミニスターズ・ノース鉄鉱床の新規権益取得について

伊藤忠商事は9月9日、BHP Group Limitedが保有するMinisters

North Iron Ore Depositの一部権益を取得する事で合意し、関連契約書署名致した。

同時に三井物産も、本鉱床の一部権益を取得する事でBHP社と合意しており、取得後の権益比率は伊藤忠商事8%、三井物産7%、BHP社85%となる。