The SF-Chem transaction is part of Clariant's strategy to sell

businesses that are outside its core activities. Last year the company

began a far-reaching Transformation Program that includes selling

several non-strategic businesses, cutting costs and making

sustainable competitiveness improvements.

Syngenta announced today that it is selling its 75

per cent stake in the Swiss chemical company SF-Chem to the Zurich-based

private equity firm Capvis. The remaining 25 per cent

stake held by Clariant is also being sold to Capvis. The total consideration

for the transaction is CHF81 million ($64 million), of which

Syngenta’s share is CHF59 million

($46 million), plus an additional performance-related component.

“It has become increasingly clear that our

investment in SF-Chem is no longer core“, said Christoph Mader,

responsible for Syngenta in Switzerland.

SF-Chem supplies customers in the chemical industry, in

particular in the pharmaceutical, agrochemical and speciality

chemicals industries. The company, founded in 1917, has its head

office and production facilities at Pratteln in Basel,

Switzerland.

SF-Chem is pursuing a growth strategy with its independently

operated business units Chemicals and Custom Manufacturing in

order to ensure an independent worldwide market position.

・

Chemicals: sulfur- and

chlorine-based intermediates.

・

Custom Manufacturing: development

of custom-tailored, specific solutions for the

pharmaceutical, agrochemical and speciality chemicals

industries.

With this move, Dyneon continues to build on its long-term

commitment to the worldwide fluoropolymer business, effectively

strengthening its product availability and reinforcing its

ability to supply product globally. Under this arrangement, which

is the first of a series of cooperative projects planned between

the companies, Dyneon will be able to better serve and support

its customers.

Dyneon, a 3M company, is one of the world's leading fluoropolymer

producers with operations or representation in more than 50

countries. Headquartered in Oakdale, Minn., Dyneon employs more

than 800 people globally who are dedicated to customer service,

technical and sales support, marketing, research, application

development, and production.

Transformational merger

of Hexal and Eon Labs with Sandoz strengthens market

positions globally, achieving top positions in key

markets, particularly US and Germany

・

Significantly broadened

product portfolio

・

One of the largest

pipelines in industry covering most generic opportunities

・

Best-in-class

development teams with proven record of being first to

market

・

Leadership in high-value

delivery technologies and biogenerics

・

Hexal and 67.7% of Eon

Labs acquired for EUR 5.65 billion

・

Tender offer for

remaining Eon Labs shares to be launched for USD 31.00

per share

・

Cost synergies of USD

200 million per year expected within three years after

closing, 50% of which to be realized within 18 months

・

Transactions to be

accretive to earnings within 12 months of closing

Quadrant has signed an

agreement with Menasha

Corporation

to purchase its Poly Hi Solidur, Inc. business, the world's leading

manufacturer of ultra-high molecular weight

polyethylene (UHMW-PE) semi-finished products for machining and fabrication.

The purchase price of approximately US$ 82 million in cash plus

the assumption of US$ 3 million of capitalized leases will be

financed from existing liquid funds and by increasing bank

borrowings by about 90 million Swiss francs. An increase in share

capital is not planned. The transaction will be completed in

August of this year. This external growth step is the

second-largest in Quadrant’s history and significantly

extends the company’s product range and its global

leadership in the market for engineering plastic products.

Poly Hi Solidur, based in Fort Wayne, Ind., US, operates

production facilities in the USA, Germany, France, the UK, Japan

and South Africa, and has dedicated R&D, sales and business

development resources among its workforce of over 1000 employees

worldwide. In 2004, the company posted total sales of US$ 169

million, approximately two-thirds of which were generated in the

US.

UHMW-PE products display very high non-stick characteristics

similar to Teflon(R) and high resistance to corrosion from

chemicals and to abrasive environments such as sand and slurries.

In machined and fabricated part form, their uses include

applications in material handling, agricultural, power

transmission and food processing machinery, as well as in medical

devices, shipping and recreational equipment. Poly Hi Solidur’s branded UHMW-PE products include

the well-known TIVAR(R) and QuickSilver(R) trademarks.

STERLING CHEMICALS, INC.

announced that it was exiting the acrylonitrile business

and related derivative operations. The Company's decision was based

on a history of operating losses incurred by its acrylonitrile

and derivatives business, and was made after a full review and

analysis of the Company's strategic alternatives.

Based in Houston, Texas, Sterling Chemicals, Inc. manufactures a

variety of petrochemical products at its facilities in Texas City,

Texas.

Sterling

Chemicals

We manufacture styrene, acetic acid and plasticizers at our

Texas City, Texas facility.

Styrene

Percent of Total North American Capacity 11%

North American Market Position by Capacity 4

Acetic Acid

Percent of Total North American Capacity 17%

North American Market Position by Capacity 3

Plasticizers

Percent of Total North American Capacity 9%

North American Market Position By Capacity 3

Canada seeks

investment in oil, petrochemicals from Alberta sands

Aromatics would be

extracted from raw bitumen contained in the oil sands, while

olefins would be cracked from naphtha to be produced from

synthetic crude oil, which in turn would come from bitumen as

well.

In a feasibility

study presented at a seminar to a group of Japanese delegates,

Plessis estimated that a production capacity of 300,000 b/d of

bitumen could support a worldscale steam cracker with ethylene,

propylene and butadiene capacities of 2,800 mt/day (1 million

mt/year), 1,600 mt/day, and 270 mt/day, respectively.

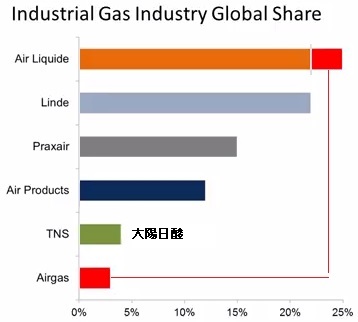

BOC, one of the world's

largest industrial gases companies, is expanding its carbon

dioxide (CO2) capacity with a new plant in Volney, New York. The

plant will be the first CO2 plant built in the Northeast in

nearly two decades and will be the only CO2 plant in the region.

BOC will build the

600 ton a day plant at the Permolex International/NEB ethanol

plant,

expected to begin operating in December 2007, and which will be

housed in a former brewery in the Riverview Business Park, some

25 miles north of Syracuse.

When BOC’s plant comes online next year it

will capture

ethanol’s by-product, CO2,

purify it and liquefy it for sale to BOC customers. Those

customers, major food and beverage companies and chemicals

manufacturers are located throughout New York, New Jersey,

Pennsylvania and New England.

2006/3/6 Linde

Recommended cash offer by

Linde for BOC

Linde AG, Wiesbaden/Germany, has agreed to make a pre-conditional

offer to acquire the entire share capital of The

BOC Group plc,

Windlesham/UK, for 1,600 pence in cash per share. The board of

directors of BOC intends to recommend BOC shareholders to accept

the offer.

The making of the offer is subject to the satisfaction or waiver

of European and US competition authority clearance pre-conditions

and the offer is subject to the requisite approval of BOC's

shareholders and the English Courts. Given the complementary

product portfolios of both companies, Linde expects that the

pre-conditions can be satisfied. Linde currently anticipates this

will occur by the end of May 2006. If the pre-conditions are

satisfied by that time, the transaction is expected to be

completed in the third quarter of 2006.

Following the acquisition, Linde will be one of the world's

leading industrial gases and engineering groups with combined gas

and engineering sales of approximately Euro 11.9 billion.

The funds necessary for the acquisition will be provided under a

credit facility entered into with Commerzbank AG, Deutsche Bank

AG, Dresdner Bank AG, Morgan Stanley International Limited and

The Royal Bank of Scotland plc. The credit facility will be

refinanced through a combination of a capital increase in an

amount of Euro 1,4 to 1,8 billion, hybrid capital (1,2 to 1,6

Euro billion), the issue of bonds, bank loans and the divestment

of selected activities. It is Linde's intention to maintain an

investment grade rating for the combined group.

2006/6/6 Linde

European Commission

approves Linde’s acquisition of BOC

The European Commission has approved the acquisition by Linde

AG, Wiesbaden, of The BOC Group plc, Windlesham, UK. The

approval is subject to certain conditions. The conditions

require the divestiture of Linde’s gas business in the UK, BOC’s gas activities in Poland and

contracts with Linde’s ethylene oxide customers in

the UK and Ireland. These divestitures correspond to a sales

volume of approximately 160 million euros.

In addition, Linde committed to transfer certain contracts

with helium suppliers and to sever, to an extent agreed with

the Commission, joint ventures between BOC and Air Liquide in

the Asia/Pacific region, either by selling BOC’s shareholding or by acquiring

Air Liquide’s shareholding.

“The approval from the European

Commission is a key step towards a merger with BOC,”

confirmed Prof.

Wolfgang Reitzle, President and CEO of Linde AG. “We expect the transaction to

be closed in the course of the third quarter of 2006. The

extent of the Commission’s conditions is in line with

our expectations and we will comply promptly with these

conditions.”

2006/7/18 Linde

U.S. Federal Trade

Commission clears Linde’s proposed acquisition of BOC

The U.S. Federal Trade Commission (FTC) has cleared the

proposed acquisition by Linde AG, Wiesbaden, of The BOC Group

plc, Windlesham, UK.

The clearance is subject to certain divestitures to address

FTC concerns relating to atmospheric gases and wholesale bulk

liquid helium. As a condition to FTC clearance, Linde has

agreed to divest eight air separation units in the United

States. It has also agreed to divest

three liquid helium purchase agreements with suppliers in the

United States, Russia, and Poland as well as associated

assets. These

divestitures correspond to a sales volume of approximately

180 million euro in the year ended December 31, 2005.

"We are pleased to confirm that each of the

pre-conditions to the making of the Offer has now been

satisfied," said Prof. Wolfgang Reitzle, President and

CEO of Linde AG. "This is a milestone on our way towards

the merger with BOC. We will swiftly take the next steps to

implement the transaction and look forward to our joint

integration process with BOC."

The Offer to the BOC shareholders will shortly be launched,

by means of the posting of the scheme document. The consent

of the High Court to the despatch of the scheme document has

been obtained. Completion of the Offer is expected in

September 2006.

Teknor Apex Company is a

privately-held company founded in 1924 and headquartered in

Pawtucket, Rhode Island. Our seven divisions and two subsidiaries

employ over 2000 people in 10 locations in the United States, one

in Singapore, and one in the United Kingdom.

Teknor Apex

entered the Far Eastern market in 2001 when it bought

Singapore Polymer Corporation, which now compounds the

full range of TPEs in Singapore.

The company's aim is to be able to supply

global companies anywhere in the world with locally

produced materials to identical

specifications. To that end it plans to open

its European plant in 2008 - it is being coy about

where the plant will be, and the Chem Polymer Oldbury

site is not the only possibility - and says that at about

the same time it will start up a

TPE plant in China.

Teknor Apex supplies TPE compounds under six trade names

that represent different technologies, including di- and

tri-block hydrogenated styrene block copolymers (Tekron,

Elexar, and Monprene), thermoplastic polyolefin blends

(Telcar), thermoplastic vulcanisates (Uniprene), and

over-moulding compositions designed to bond to diverse

polar substrates (Tekbond).

--------

Teknor Apex

Company traces its origins to Apex Tire

Company

which was started in Providence, Rhode Island in 1924.

Alfred A. Fain, a retired wholesale grocery executive,

and his son-in-law, Albert Pilavin, grew this tire sales

and recapping business until it had expanded to include

16 retail tire stores along the East Coast.

Today the Rubber Division of Teknor Apex has a healthy

business mixing rubber compounds for outside customers

and molding its own products such as rubber floor mats.

In 1949 the Company began the production of vinyl

compounds

as a result of a shift in the wire and cable industry

from rubber to vinyl materials. Apex Rubber also began

manufacturing vinyl resin and plasticizers as the vinyl

compounding part of the business grew.

Today Teknor Apex is a leading custom compounder of PVC

and thermoplastic elastomer products used in many

industries such as wire and cable, medical, automotive,

building materials and appliances.

Vinyl garden hose production was begun in the Pawtucket,

RI plant in the late 50s as an outgrowth of the company's

vinyl production. The Lawn and Garden

business at

Teknor Apex has also grown over the years and Teknor Apex

is now one of the major manufacturers of garden hose in

the United States.

The Massachusetts

plant produced chemicals and PVC resin.

In 1959 Teknor Apex began selling colorants

for plastics

to customers buying its vinyl compounds.

Through acquisitions over the years, in 1981 this

operation became Teknor Color Company, a wholly owned

subsidiary of Teknor Apex Company.

Vinyl

Thermoplastic

Elastomer

Teknor Color Company

Chemicals

Specialty

Compounding

Lawn & Garden

Commercial Products

The Vinyl

Division of

Teknor Apex is one of the world's leading suppliers of specialty

PVC compounds.

The

Thermoplastic Elastomer Division of Teknor Apex has built its

worldwide TPE leadership on more than 75 years experience with

flexible and elastomeric polymers.

Headquartered in Pawtucket, Rhode Island, Teknor Apex also

operates thermoplastic elastomer facilities in St. Albans,

Vermont; Brownsville, Tennessee; Henderson, Kentucky; and in

Singapore.

With strategically

located plants across North America and one in Singapore, Teknor Color

Company provides

colorants for the plastics industry worldwide. We offer a full

line of custom and standard colors and additives as well as

special effects for all processes.

Chem Polymer is an engineering

thermoplastics compounder which produces reinforced, filled

and specially modified compounds of nylon 6 and 66, acetal, PBT

and PET for automotive, appliance, electrical, electronic and

other applications.

Teknor

Specialty Compounding is a diversified toll and custom

manufacturer of thermoplastic compounds and additive blends. We

are a resource for customers requiring an independent,

confidential provider of production capacity, formulating

experience and process expertise.

Teknor Apex Acquires Chem

Polymer, International Supplier of Engineering Plastics Compounds

with Plants in UK and USA

Teknor Apex Company today

purchased the UK and US engineering thermoplastics compounding

businesses of Chem Polymer, which is a leading supplier to

customers throughout Europe and the Americas and has a growing

presence in Asia. Chem Polymer will operate under its existing

management as a distinct entity within Teknor Apex, retaining the

Chem Polymer name and a workforce of 150.

Until now a member of the UK-based Chem Polymer Group (formerly

BIP Group), Chem Polymer produces reinforced, filled, and

specially modified compounds of nylon 6 and 66, acetal, PBT, and

PET for automotive, appliance, electrical, electronic, and other

applications. It operates two plants in the UK and one in the

USA, with combined annual capacity of 30,000 metric tons

(66,000,000 lb.).

Teknor Apex Co., a

U.S.-based compounder of specialty PVC, thermoplastic elastomers

and color concentrates, plans to start a European TPE compounding

operation in 2008, officials said at Fakuma 2006.

Teknor Apex plans

to install a small compounding operation next year in the

Oldbury, England, factory of Chem Polymer, according to Andre Toczek, sales

and marketing manager of the European operation.

Teknor officials have not

decided the location of the full-scale TPE production, although

Oldbury is one option, Toczek said Oct. 19 at the show.

January 9, 2007 RTP

RTP Company Announces Long Fiber Thermoplastics Availability at

China Facility

RTP Company, a global leader in specialty compounds, has added

multiple long fiber-reinforced

thermoplastic (LFRT)

production lines at its Suzhou, China manufacturing facility. The

long glass fiber compounds are based on various resin systems

including nylon and polypropylene.

“The

new LFRT lines will support our rapidly-growing automotive and

industrial customer base in China along with offering long fiber

technology to other markets for applications requiring higher

strength at lighter weights,” said Joe Kluck, Executive Vice

President at RTP Company.

RTP Company’s 16,000 square meter (170,000

square feet) manufacturing plant in Suzhou, China was opened in

December 2005. The state-of-the-art facility offers a full

complement of customer support, product development, and

technical service.

RTP Company significantly expanded its LFRT capabilities earlier

this year with the opening of a long fiber facility near its

Winona, Minnesota headquarters. RTP Company also installed

additional long fiber lines at several of its worldwide

operations in 2006 and introduced a broader long fiber product

offering.

Long Fiber Compounds are often used to replace metals and

consequently have become one of the fastest-growing materials in

the thermoplastic industry. They offer excellent mechanical

properties and their high strength-to-weight ratios result in

parts that can withstand heavy loads over long periods of time,

even in elevated temperatures.

ABOUT RTP COMPANY

RTP Company, headquartered in Winona, Minnesota, is a global

leader in specialty thermoplastic compounding. The company has

eight manufacturing plants on three continents, plus sales

representatives throughout North America, Europe, and

Asia/Pacific. RTP Company's engineers develop and produce custom

compounds in over 60 different engineering resin systems for

applications requiring color, conductivity, flame retardancy,

high temperature, structural, elastomeric and wear resistant

properties.

Mexico's PVC producer

Mexichem eyes takeover of Pemex's VCM plant

Mexico City-based

chemicals group, Mexichem, whose recent acquisitions have

made it the biggest producer of PVC in

Latin America,

aims to break a production bottleneck by taking control of state Pemex's VCM plant, Enrique Ortega, Mexichem's

investor relations manager said Monday.

"We supply the plant with 90% of the

chlorine it

uses and buy 70% of its VCM output," Ortega told Platts.

"It's natural that we would want to acquire it and the law

allows us to do so." VCM is classified as a secondary

petrochemical to which Pemex's state monopoly does not apply.

The

Pajaritos VCM plant has

been a thorn in Mexichem's flesh for some time. In 2002, Pemex

announced the award to Spain's Duro Felguera of a $74 million

contract for an expansion of the plant's capacity from 200,000

metric tons/year to 405,000 mt/year. The expansion project took

much longer than programmed, forcing Mexichem and others to

import VCM in the meanwhile, and the expansion of production

capacity appears to have fallen far short of target. Last year

the plant produced 209,000 mt/year of VCM.

In February, Mexichem announced the acquisition of two Latin

American companies -- Costa Rica-based Grupo Amanco, which makes PVC piping for water

systems, and Petroquimica Colombiana (Petco), a Colombia-based producer of PVC

resins. The addition of Amanco and Petco to Mexichem's

fast-growing portfolio of affiliates should double the group's

revenues to $2.4 billion this year, Ortega said.

Clariant sells Custom Manufacturing Business to International

Chemical Investors Group

Clariant today announced the sale of its Custom

Manufacturing Business to International Chemical Investors Group

(ICIG) for

an undisclosed transaction value. The sale is the latest step in

Clariant’s strategy to focus on its core

competencies in colors, surfaces and performance chemicals.

Clariant’s Customer Manufacturing Business

supplies a wide range of intermediates and actives ingredients

for the agrochemicals, pharmaceuticals and polymers industries.

At closing, the new autonomous entity will be one of the world’s leading suppliers to the

agrochemicals industry with production sites in Germany and the

US. In 2006, the Custom

About International Chemical Investors

International Chemical Investors is an investment group focusing

on mid-sized chemical businesses, preferably subsidiaries of

large corporations, which are considered non-core, with leading

positions in niche markets, operating in competitive

environments. Including the newly acquired Clariant businesses,

ICIG will operate 14 production facilities located in Germany,

the United States, France, Belgium, Ireland and Poland with total

sales of close to Euro 500 million and more than 2,500 employees.

CVC to Buy Chemical

Seller Univar for EU1.52 Billion

CVC Capital Partners Ltd.

agreed to buy Univar NV of the Netherlands for 1.52 billion euros ($2.07 billion) to gain the largest distributor

of chemicals in the U.S.

Europe's No. 2 buyout

firm will purchase Univar for 53.50 euros a share, the companies

said in a statement today. That's 37 percent more than Friday's

closing price for Univar, which buys bulk chemicals and then

sells them to 250,000 industrial users.

CVC's bid comes less than

three months after Rotterdam- based Univar bought

Chemcentral Corp. of Illinois to boost U.S. sales 40 percent.

London-based CVC said it backs expansion in the world's biggest

economy, which grew at its slowest pace since the end of 2002 in

the first quarter, and also plans to fund further acquisitions in

Europe, Asia and the Middle East.

Univar has 8,000 employees and more than

200 chemical- distribution centers in the U.S., Canada, Europe

and Asia, it said in the statement. The majority of the company's

products are commodity chemicals bought in bulk and then processed,

blended and sold to clients in industries ranging from

agriculture and drugs to forestry, food and electronics.

CVC is investing 10

billion euros it has amassed in the past two years. The Univar

deal comes five days after the 800 million-euro

purchase of Taminco NV, a Belgian maker of chemical ingredients

for the pharmaceutical industry. Dutch investment firm AlpInvest

Partners NV sold Taminco in an auction.

CVC was founded in 1981

as Citicorp's European private- equity arm before its managers

bought their independence in 1993. Run by Michael Smith, who

joined from Citibank in 1982, the firm has about $24 billion of

funds. It already owns more than 40 companies with more than

300,000 employees and revenue in excess of 38.5 billion euros,

according to its Web site.

Hexcel Corporation, in

conjunction with Tianjin Xeda Administrative Committee, has today

announced further details of its plans to build a new prepreg

plant in China.The new facility is intended to

meet the strong demand for composites used in wind turbines.China is

experiencing major growth in its wind energy market and the

country plans to double the amount of energy it obtains from

renewable sources by 2020; a strategy that will require a major

increase in the number of wind power plants in the country.

With the support of Xeda,

Hexcel has secured a total floor area of 30 000m2 site in

Tianjin, close to the facilities of major wind power customers.

The plant building area will occupy approximately 8,000m2 and

manufacture HexPly® epoxy resin

prepregs,

primarily for wind energy and industrial applications.Production at the

new facility will commence in summer 2008.

Prepreg is

fiber-reinforced resin system that cures under heat and pressure

to produce structures with a very high strength to weight ratio.Prepreg is widely

used in the wind energy industry where its outstanding strength

and low weight have enabled turbine blades to grow to today’s giant proportions.

HexPly® prepregs are specially

formulated resin matrix systems, that are reinforced

with man-made fibers such as carbon, glass and aramid.When cured at

elevated temperatures, the themoset resin undergoes a

chemical reaction that transforms the prepreg into a solid

structural material that is highly durable, temperature

resistant, exceptionally stiff andlightweight.

Rio Tinto notes the

recent announcement from BHP Billiton involving a proposed

acquisition of Rio Tinto. Under this proposal each Rio Tinto

share would be exchanged for three BHP Billiton shares.

The Boards of Rio Tinto

have given the proposal careful consideration and concluded that it significantly

undervalues Rio Tinto and its prospects. Accordingly, the Boards have

unanimously rejected the proposal as not being in the best

interests of shareholders.

Rio Tinto will continue

to focus on the implementation of its well articulated strategy,

including integrating Alcan operations.

A merger would create

a base metals colossus with powerful positions in coking

coal, iron ore, copper and aluminium. BHP's offer - three BHP

shares for every Rio share, which values the bid at more than $140

billion

on current prices - was rejected by Rio at a board meeting

held earlier this week to consider the proposal. Rio shares

gained 956p, or 22 per cent, to £52.96 in response to news of

BHP's interest, while BHP fell 100p, or 5.6 per cent, to £16.56.

Albemarle to Expand

Antioxidant Production in China

Strategic move will

further strengthen position in the China plastics additives

marketplace

Albemarle Corporation, a

leading global supplier of antioxidants for polymers, lubricants,

fuels and biofuels, announced today that its Board of Directors

has approved a project to more than double the

antioxidant production capacity of Shanghai Jinhai Albemarle Fine

Chemicals Co., Ltd.,

part of the "Jinhai Albemarle" manufacturing joint

venture in which Albemarle gained a majority ownership stake last

year.

This strategic expansion

will allow Jinhai Albemarle to maintain its market position as

the leading manufacturer and supplier of polymer antioxidants in

China.

2008/6/22

polymer-age.co.uk

Cabot

to manufacture in the Middle East

Carbon

black masterbatch producer Cabot Corporation is to start making

masterbatch in the Arabian Gulf. It is to build a plant in the

Jebel Ali Free Zone, Dubai with an

initial capacity of 25,000tonnes

with provision to expand to

75,000tonnes.

Output

from the plant will be sold in the Middle East, Europe and Asia

Pacific. The key markets for black masterbatch are in PE and PP

compounds for building infrastructure, water supply, electricity,

and telecommunications.

By

2010 the Middle East is expected to produce one-fifth of the

world's polyethylene and polypropylene.

2008/5/28 Cabot

Cabot Corporation to

Build Masterbatch Facility in Dubai

Cabot Corporation

announced today that it intends to build a carbon black

masterbatch manufacturing facility in the Jebel Ali Free Zone,

Dubai. The plant will have an initial production capacity of

25,000 tons per year with provision to expand to 75,000 tons in

the future. Cabot has secured a plot of land and construction

will begin later this calendar year, with production scheduled to

start in the fall of 2009.

The state-of-the-art

manufacturing facility will include the latest environmental and

manufacturing technologies to ensure production of high-quality

masterbatch products. Laboratories, administration offices,

production and packaging will all be located within the building.

The Dubai plant will

allow Cabot to better meet the increasing demand of its customers

in the Middle East, Europe, and Asia Pacific regions. In recent

years, the Middle East has become a major producer of polyolefins

and downstream compounds and by 2010 is expected to produce

one-fifth of the world's polyethylene (PE) and polypropylene

(PP).

Cabot Vice President and

General Manager for the Performance Segment, Sean Keohane said,

"Within the Middle East there is already strong demand for

PE and PP compounds for use in building infrastructure for water

supply, electricity, and telecommunications projects. These are

key markets for carbon black masterbatch. This new site will

offer significant quality and service advantages to Middle East

producers who are global exporters of masterbatch

compounds."

2008/10/3 Ferro

Ferro Announces Agreement

to Sell Fine Chemical Business

Ferro Corporation (NYSE:

FOE) announced today that it has signed an asset purchase

agreement with Novolyte Technologies LP, an affiliate of Arsenal

Capital Management LP, to sell its Fine Chemicals business for

$66 million in cash.

"This sale is

consistent with our vision of focusing Ferro's businesses around

our core capabilities of particle engineering, formulation, color

and glass science, and our deep understanding of customer

applications," said Ferro Chairman, President and Chief

Executive Officer James F. Kirsch. "The decision to sell the

business is a result of a regular review of our business

portfolio. Fine Chemicals consists of a number of smaller

businesses that do not effectively leverage the scale of Ferro's

core performance materials operations. I am confident that the

Fine Chemicals business will continue to pursue many exciting

opportunities under its new owners. At the same time, Ferro will

benefit from additional liquidity and balance sheet flexibility

as proceeds from the sale are used to reduce debt."

The Fine Chemicals

business produces electrolytes used in the manufacture of lithium

batteries, specialty solvents, and phosphines and also does

contract manufacturing of fine chemicals. It recorded 2007

revenues of approximately $55 million and currently employs

approximately 140 employees who will be transferred to Novolyte

as a result of the sale. The business includes manufacturing

facilities in Baton Rouge, Louisiana and Suzhou, China.

The agreement is subject

to normal closing conditions and the sale is expected to close in

the fourth quarter of 2008. KeyBanc Capital Markets served as

Ferro's financial advisor and investment banker for this

transaction.

About Ferro Corporation

Ferro Corporation

(http://www.ferro.com) is a leading global supplier of

technology-based performance materials for manufacturers. Ferro

materials enhance the performance of products in a variety of end

markets, including electronics, solar energy, telecommunications,

pharmaceuticals, building and renovation, appliances, automotive,

household furnishings, and industrial products.

Headquartered in

Cleveland, Ohio, the Company has approximately 6,300 employees

globally and reported 2007 sales of $2.2 billion.

Lilly to Acquire ImClone

Systems in $6.5 Billion Transaction Creates a Global Leader in

Oncology Biopharmaceuticals Boosts Oncology Pipeline With Up

to Three Promising Targeted Therapies in Phase III in 2009

Eli Lilly

and Company and ImClone Systems Inc. today announced that the boards

of directors of both companies have approved a definitive merger

agreement under which Lilly will acquire ImClone through an all

cash tender offer of $70.00 per share, or approximately $6.5 billion. The offer represents a premium of

51 percent to ImClone's closing stock price on July 30, 2008, the

day before an acquisition offer for ImClone was made public.

ImClone's board recommends that ImClone's shareholders tender

their shares in the tender offer. Additionally, certain entities

associated with ImClone's chairman, Carl C. Icahn, holding

approximately 14 percent of ImClone's outstanding common stock,

have agreed to tender their shares in the tender offer.

Sep 22, 2011 (Datamonitor via COMTEX)

Williams to expand Geismar olefins production

facility

Williams, an integrated

natural gas company focused on exploration and production, midstream

gathering and processing, and interstate natural gas transportation, has

announced that its board of directors has approved an expansion of its

Geismar olefins production facility.

The expansion will increase the facility's ethylene production capacity

by 600 million pounds per year to a new annual

capacity of 1.95 billion pounds. It is expected to

be placed into service in the third quarter of 2013, the company said.

Located south of Baton Rouge, La., the Geismar facility is a

light-end natural gas liquid (NGL) cracker with current volumes of 37,000

barrels per day (bpd) of ethane and 3,000 bpd of

propane and annual production of

1.35 billion pounds of ethylene. The facility also

produces propylene, butadiene and debutanized aromatic

concentrate (DAC). Williams owns 83.3 percent of the Geismar facility and

operates the plant.

"The shale gas revolution in the US, coupled with continued strong crude oil

prices, has given US-based ethylene manufacturing a tremendous cost advantage

over many other supply regions," said Rory Miller, president of Williams'

midstream business. "The results are a revitalized North American petrochemical

business and a US ethylene market short of supply.

"This expansion will serve petrochemical companies by adding 600 million pounds

per year of new ethylene supply to the market," Miller said. "It will also add

to Williams' growing large-scale infrastructure serving the petrochemical

industry in the Gulf Coast region and help balance our lengthening ethane

position."

The expected capital spending on the Geismar expansion is a range of $350

million to $400 million in 2012-13. These amounts will be included in the

company's 2012-13 capital expenditure guidance to be released in conjunction

with third-quarter 2011 financial results, the company added.

--------

An integrated natural gas company, Williams

produces, gathers, processes and transports clean-burning natural gas to

heat homes and power electric generation across the country.

Williams' olefins business provides

customers in the petrochemical industry a full suite of products and

services.

Gulf Coast Olefins

The Geismar, La. facility annually produces approximately 1.3 billion pounds

of ethylene and 90 million pounds of polymer grade propylene. Also in

Louisiana, the olefins team is responsible for the ethane transportation

business consisting of approximately 200 miles of pipelines, as well as a

refinery-grade propylene splitter.

Canadian Olefins

Williams’ Canadian olefins business extracts natural gas liquids and

olefins from oil sands refining near Fort

McMurray, Alberta. The liquids are then fractionated into various products

at a Williams facility near Redwater, Alberta. Williams also has a business

office in Calgary.

Cryogenic Liquids Extraction Plant

Located Near Fort McMurray

An environmentally-friendly project

as it reduces sulphur emissions and other green house gases

Extracts natural gas liquids (NGLs)

from coker off-gas produced from an oil sands plant

Coker off-gas includes olefins such

as propylene which is typically produced through ethane or propane

cracking

Olefins Fractionation Plant Located

Near Edmonton

Only olefinic fractionator in

Western Canada

Fractionates NGL mix from Fort

McMurray

On a yearly basis, produces

approximately 2.4MM bbls of propane, 140MM lbs of polymer grade

propylene, 1.10MM bbls of butane/butylene mix and 230K bbls of olefinic

condensate

October 17, 2011 PolyOne

PolyOne Expands Globalization with New Middle

East Joint Venture

PolyOne Corporation, a premier global provider of specialized polymer materials,

services and solutions, today announced an agreement with

E.A. Juffali & Brothers Company Limited to form a joint venture that will

enable PolyOne to expand its Global Color, Additives and Inks business into the

Middle East. The new joint venture will be 51% owned by PolyOne and will be

based in Jeddah, Saudi Arabia.

“I am pleased to announce our new agreement, which strengthens our relationship

with a key business partner to drive profitable growth in the Middle East,” said

Stephen D. Newlin, chairman, president and chief executive officer of PolyOne.

“Juffali brings local expertise and years of running successful businesses in

the region, while PolyOne is providing the formulating technology and material

science to market new, innovative solutions.”

The joint venture will be investing in a new manufacturing facility focused on

the production of specialty color concentrates with the potential for expansion

into other product lines in future phases. The initial investment is expected to

be approximately $14 million and will take place over the next nine to twelve

months with local production forecasted to come on-line in late 2012.

The agreement follows PolyOne’s October 3, 2011 announcement that it will

acquire ColorMatrix Group, a

leading global innovator of additives, liquid colorants and fluoropolymers.

About PolyOne

PolyOne Corporation, with 2010 revenues of $2.6 billion, is a premier provider

of specialized polymer materials, services and solutions. Headquartered outside

of Cleveland, Ohio USA, PolyOne has operations around the world. For additional

information on PolyOne, visit our Web site at www.polyone.com.

About E.A. Juffali & Brothers Company Limited

E.A. Juffali & Brothers Company Limited is an established conglomerate in Saudi

Arabia participating in numerous joint venture relationships with multi-national

companies who are leaders in their respective industries such as Dow Chemical

and DuPont.

---------

October 03, 2011 PolyOne

PolyOne Accelerates Specialty Growth with

Agreement to Acquire ColorMatrix Group

PolyOne Corporation, a premier global provider of specialized polymer materials,

services and solutions, today announced an agreement to acquire

ColorMatrix Group, Inc., the leading global

innovator in liquid colorants, additives and fluoropolymers.

“I am extremely pleased to announce we’ve reached an agreement to acquire

ColorMatrix, an exceptional and unique specialty company,” said Stephen D.

Newlin, chairman, president and chief executive officer, PolyOne Corporation.

“Much like our acquisition of GLS in 2008, ColorMatrix is a game-changer for

PolyOne. With the addition of ColorMatrix, more than 50 percent of PolyOne’s

operating income will now be derived from our specialty businesses, compared to

only 2 percent in 2005.”

ColorMatrix is the leading manufacturer of performance-enhancing specialty

additives, liquid colorant and dosing technologies that serve diverse niche

markets, such as rigid beverage and food packaging, performance molding and

fiber. The company’s leadership position in technology is evidenced by an IP

portfolio of 162 patents and 107 pending applications worldwide. Its solutions

in packaging, in particular, offer customers exceptional performance attributes

such as increased product shelf life, taste preservation and improved

recyclability.

Further, ColorMatrix is a leading global provider of colorant for fluoropolymers

and provides specialty additives that support fluoropolymers’ unique

high-performance properties such as lubricity, high-level heat insulation,

static dissipation and x-ray opaqueness. Through its April 2011 acquisition of

Gayson, ColorMatrix expanded its portfolio to include short turnaround, custom

color dispersions used in silicone processing for a broad range of medical,

consumer and automotive applications.

Under the leadership of CEO John Gelp and a strong management team, ColorMatrix

achieved sales and EBITDA of approximately $196.8 million and $43.6 million

respectively for the 12 months ended June 30, 2011.

“Since 2002, ColorMatrix has organically increased EBITDA at an annualized

growth rate of 16 percent, and our purchase price of $486 million recognizes the

earnings and growth potential of this specialty business,” said Newlin. “We

believe we can accelerate this growth by leveraging our global scale and through

additional investment in commercial resources, just as we’ve done with GLS.”

“Not only will the acquisition of ColorMatrix accelerate our specialization

strategy, it also expands our geographic presence in Asia and Brazil and creates

an entry point into Russia,” said Robert M. Patterson, executive vice president

and chief financial officer. Approximately 70 percent of ColorMatrix’s revenues

are outside North America.

PolyOne intends to finance the purchase price of $486 million, which includes

transaction tax benefits of $10 million, with a combination of cash on hand and

the addition of approximately $300 million of long term debt. The acquisition is

being made on a cash free, debt free basis, and the purchase price is subject to

a customary working capital adjustment and other closing conditions.

“Net of interest expense on the long term debt, and the incremental investments

in commercial resources, we expect ColorMatrix to be modestly accretive to

earnings in 2012 ($0.02-$0.03 per share) and to add approximately $0.10-$0.12

per share in 2013,” added Patterson.

This acquisition is subject to regulatory approvals and is expected to close

late this year. PolyOne management will discuss the acquisition in more detail

during its regularly scheduled third quarter earnings conference call to be held

on October 26, 2011.

About ColorMatrix

ColorMatrix Group Inc., based in Berea, Ohio, is a leading specialty provider of

innovative liquid colorants and additives business that serves diverse segments,

including rigid beverage and food packaging, industrial extrusion, performance

molding, wire, cable, fiber, and silicone rubber markets. ColorMatrix has

operations, R&D capabilities and customer reach throughout the globe. For

additional information on ColorMatrix, visit its Web site at www.colormatrix.com.

December 2, 2013

Rockwood to Acquire 49%

Interest in Talison Lithium through a Joint Venture with Chengdu Tianqi Industry

Group

Provides ownership in the

world’s largest and richest spodumene sourceリチア輝石

of lithium リチウムとアルミニウムを含む単斜輝石

Strengthens further ROC’s #1

position as a leading global integrated producer of lithium compounds and

chemicals

Delivers immediate and

significant accretion to ROC’s 2014 earnings per share

Enables a partnership with

Tianqi, China’s leading lithium company

Rockwood Holdings, Inc.

announced today that it entered into a joint venture ("JV") with Chengdu Tianqi

Industry Group ("Tianqi"成都天齊實業集團) giving Rockwood a 49%

ownership interest and Tianqi a 51% interest in

Talison Lithium Pty Ltd. This transaction is expected to close during the

first quarter of 2014, following receipt of regulatory approvals.

Rockwood (49%) and Chinese

lithium producer Chengdu Tianqi Group (51%) will form a joint venture to

acquire Talison from its current owners (Windfield is the Holdco of Talison

Lithium Pty Ltd.)

At close, it is expected that

Rockwood and Tianqi will contribute equity of $196 million and $204 million,

respectively. In addition, Rockwood will also provide to the joint venture a

two-year secured loan of up to $670 million at 8% interest. Rockwood will grant

Tianqi a three-year call option to invest from 20% to 30% in the equity of

Rockwood Lithium GmbH, the European arm of

Rockwood’s global lithium business, which will be valued at 14x the last twelve

months Adjusted EBITDA.

Proceeds to the joint venture

will be used to pay off existing debt and equity holders including Tianqi Group

HK Co., Limited (a subsidiary of Tianqi) and Leader Investment Corporation (a

subsidiary of China Investment Corporation). Rockwood is expected to fund its

investment in the joint venture from cash on hand.

"With this acquisition, we have

secured access to another significant lithium reserve, in addition to our

current resources in the U.S. and Chile," said Seifi Ghasemi, Chairman and Chief

Executive Officer. "Further, not only does this complement our core lithium

business, but it also meets with all of our prior stated financial and strategic

objectives for allocation of capital in a disciplined manner to enhance economic

value for shareholders."

Lazard acted as Rockwood’s

financial advisor and Clifford Chance as legal advisor.

Talison Lithium Pty Ltd

Talison is a leading global

producer of lithium for over 25 years. Talison mines and processes lithium

bearing mineral spodumene at its operations located at Greenbushes, Western

Australia (the "Greenbushes Lithium Operations"), located approximately 250

kilometers from Perth, Western Australia. Greenbushes Lithium Operations is

estimated to be the world’s largest known reserves of lithium spodumene minerals

with a current mine life of 40 years.

Talison has a leading position

in the growing Chinese lithium concentrates market. Talison produces two

categories of lithium concentrates: (i) technical-grade lithium concentrates

which have low iron content for use in the manufacture of, among other

applications, glass, ceramics and heat-proof cookware; and (ii) a high-yielding

chemical-grade lithium concentrate which is used to produce lithium chemicals

which form the basis for manufacture of, among other applications, lithium-ion

batteries for laptop computers, mobile phones, electric bicycles and electric

vehicles.

Chengdu Tianqi Industry

Group Co., Ltd ("Tianqi")

Tianqi is a privately held

Chinese company founded in 2003. Tianqi and its subsidiaries conduct their

operations mainly from China, but have customers, business partners and

suppliers in various countries around the world, including Europe, Australia,

the United States and Japan. Its business activities are primarily conducted

through the following subsidiaries:

Sichuan Tianqi Lithium

Industries, Inc. – a Chinese company listed on the Shenzhen Stock Exchange,

engaged in the production of lithium carbonate and other lithium products

from chemical-grade lithium concentrates sourced from

Talison;

Sichuan Tianqi Industry Co.,

Ltd. – a distributor of technical grade lithium concentrates, as the sole

distributor for Talison in China;

Chengdu Tianqi Machinery –

provides spare parts and accessories for machinery and electrical equipment

used in the construction, packing and agriculture sectors; and

Chengdu Sendasun

Agricultural Machinery Co., Ltd. – undertakes research, development,

manufacturing and sales of agricultural equipment.

In June 2012, Talison

completed and commissioned a new chemical-grade concentrate processing plant

to double Talison’s production capacity to 740,000 tons per year of

concentrate (~100,000 tones lithium carbonate equivalent per annum)

Langelsheim is the largest and most

diverse production location operated by the Chemetall Group. Today's

production range covers chemicals for the surfact treatment of metals,

inorganic and organic lithium compounds and lithium metal, aircraft

sealants as well as high-purity metals and metal compounds of the elements

caesium, barium, titanium and zirkonium.

Talison Lithium is a leading global

producer of lithium.

Talison Lithium’s headquarters are in

Perth, Western Australia and the Company has over 140 employees located in

Australia, Canada, Chile and China.

Talison Lithium currently produces

lithium concentrate at its lithium mineral project in Western Australia

located in the town of Greenbushes. The lithium orebody at Greenbushes is

unique in that it contains large zones of high grade lithium ore. Lithium

has been produced from the Greenbushes operations for over 25 years and

Talison Lithium currently exports over 350,000 tonnes of lithium products

annually to a global customer base.

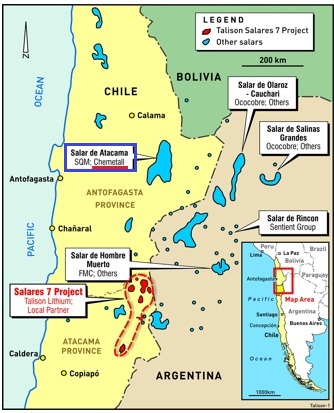

Talison Lithium also has a lithium brine

project located in the Atacama Region III, in Chile.

This prospective exploration project consists of seven salars (brine lakes

and surrounding concessions). Five of the salars are clustered within a

radius of approximately 30kms and are 100% owned by Talison Lithium and its

Chilean partners.

The Salares 7 Project

consists of seven salars (salt lakes) and playas located in the

Atacama Region of Northern Chile. Five of the seven salars are

100% owned by Talison Lithium and its Chilean partners, and

these five are clustered within a radius of approximately 30

kilometres. The salars are largely underlain and surrounded by

volcanic rocks of andesitic to basaltic affinity that make up

some of the 800 volcanoes located in the Andes Mountains of

northern Chile.

The salars are salt filled

closed basins, confined by a sequence of volcanic rocks. The

brines in the salars were formed by leaching of the host

volcanic rocks by snowmelt and rainwater run-off that

accumulated in the closed basins. Evaporation concentrated the

waters and precipited the salts which are commonly gypsum and

halite.

Talison Lithium’s exploration

program at Salares 7 has included initial drilling, transient

electromagnetic geophysical surveys and regional surface water

geochemical sampling programs. Talison Lithium has also

undertaken process test work studies to assist in designing a

processing facility for the project and collecting environmental

data.

------

August 23, 2012

Rockwood Holdings Agrees to Acquire Talison Lithium

Rockwood Holdings Inc. announced today that it has entered

into a definitive agreement with Talison Lithium Limited to

acquire all of the outstanding shares of Talison in an all-cash

transaction for C$6.50 per share for an equity purchase price of

approximately C$724 million, on a fully diluted basis (US$732, based

on an exchange rate of C$1 = US$1.011635). The Board of Directors of

Talison has unanimously recommended the transaction to Talison

shareholders. The transaction is subject to the approval of Talison

shareholders and other customary closing conditions.

Rockwood intends to finance the acquisition using existing cash on

its balance sheet and new debt financing.

Commenting on the transaction, Seifi Ghasemi, Chairman and CEO of

Rockwood, "The acquisition of Talison is the logical next step in

further strengthening our lithium business and enhancing our

capabilities. This acquisition will enable us to better serve both

our existing global customers as well as Talison's current lithium

concentrate customers in China and the rest of the world".

Lazard is acting as exclusive financial advisor to Rockwood, and

Gilbert & Tobin is acting as Rockwood's legal counsel.

In a C$724 million

cash-ready deal for Talison, Rockwood aimed

to dominate about half the world’s

lithium market, adding, roughly speaking, Talison's

30 percent market share to its 20 percent.

But Talison's chief customer in China,

Chengdu Tianqi, usurped Rockwood’s plans, eventually

making what Talison’s board deemed a superior offer worth

$847 million.

Rockwood declined to enter a bidding war.

Nov 13, 2012

Chengdu Tianqui Proposes Talison

Bid to Trump Rockwood

Chengdu Tianqi Industry Group Co., a closely held Chinese battery maker, said it

will make an offer for Australian mining company Talison Lithium Ltd. that will

exceed an agreed takeover bid from Rockwood Holdings Inc. (ROC)

Chengdu Tianqi’s Windfield Holdings unit agreed to buy or has already purchased

an aggregate 15 percent stake in Talison, the Chengdu, Sichuan province-based

company said yesterday in a statement. Chengdu Tianqi plans to submit a proposal

for the rest of the shares at a higher price than Rockwood’s bid of C$6.50

($6.50) a share, according to the statement.

Talison, based in Perth, Australia, mines ore to produce battery-grade lithium,

which analysts at Dahlman Rose & Co. say may double in demand during the next

eight years on its use in electric vehicles. Talison has the largest open-pit

mine for lithium with the highest grade ore in the world, according to Jonathan

Lee, an analyst at Toronto-based Byron Capital Markets Ltd. Chengdu Tianqi

purchases more than 90 percent of its lithium raw material from Talison, he

said.

“It’s basically vertical integration for them and securing their source of

supply,” Lee said in a telephone interview yesterday.

Talison rose 7.9 percent to C$6.96 in Toronto yesterday.

Talison dominates the market for technical-grade lithium used in the glass and

ceramics industries, he said. Tianqi is the only distributor of Talison’s

technical-grade lithium in China, according to the statement.

Australian Approval

“There’s a limited number of competitors in that space that are vastly smaller

than Talison,” Lee said.

Talison said yesterday in a statement it hasn’t received a proposal from Chengdu

Tianqi and recommends shareholders vote for Rockwood’s bid. A voicemail message

left with Princeton, New Jersey-based Rockwood wasn’t immediately returned.

Talison will be able to grow its business and continue its track record of

innovation and development in Australia, Joshua Goldman-Brown, a spokesman for

Chengdu Tianqi from public relations company Kreab Gavin Anderson, said

yesterday in an interview.

A takeover by Chengdu Tianqi would have to be approved by Australia’s Foreign

Acquisitions and Takeovers Act and may be blocked because of the uniqueness of

Talison’s resources, Lee said. Goldman-Brown declined to comment on the details

of the approval process.

Chengdu Tianqi, which also makes agricultural machinery, owns a 20 percent stake

in Quebec City-based exploration company Nemaska Lithium Inc., according to a

Nov. 1 statement from Nemaska.

Separately, Toronto-based Canada Lithium Corp. said

yesterday it agreed to a five-year agreement to supply China’s Tianjin Products

and Energy Resources Development Co. with 12,000 metric tons of battery-grade

lithium carbonate annually.

Chengdu

Tianqi Industry (Group) Co., Ltd. today announced that Windfield Holdings

Pty Ltd, a wholly-owned subsidiary of Tianqi, has entered into a definitive

agreement with Talison Lithium Limited to acquire all of the shares in

Talison that it does not already own in an all cash transaction at a price

of C$7.50 per share, by way of a scheme of arrangement (the "Transaction").

The aggregate consideration to be paid to Talison securityholders under the

Transaction is approximately C$847 million.

December 12, 2012

Tallison Lithium and Rockwood

terminate agreement

Talison Lithium Limited

and Rockwood Holdings, Inc. have agreed to terminate the scheme implementation

agreement for the proposed schemes of arrangement between Talison and its

Shareholders and Optionholders that would have resulted in all Talison

Securities being acquired by a wholly owned subsidiary of Rockwood, as announced

on August 23, 2012. Talison will pay Rockwood a C$7 million break fee.

The termination of the Rockwood

Proposal was foreshadowed in Talison’s announcement on December 6, 2012

regarding the proposed schemes of arrangement between Talison and its

Shareholders and Optionholders that would result in all Talison Securities being

acquired by Windfield Holdings Pty Ltd, an Australian incorporated wholly-owned

subsidiary of Chengdu Tianqi Industry (Group) Co., Ltd

.

17 Oct 2014 Pirelli

Pirelli and Rosneft, agreement

in the synthetic ruber sector in Nakhodka to extend to new technological partner

Pirelli and Rosneft, in the context of the agreement signed last May for the

production and supply of synthetic rubber in Nakhodka,

today reached a new agreement which calls for, on the basis of a short list, the

identification within three months of a new technological partner for the

further development of activities in the rubber sector, including

Styrene-Butadiene Rubber (SBR), in that region.

Under the terms of the MOU, Rosneft and future partner will analyze the ways in

which the joint production of synthetic rubber could be launched in Nakhodka,

while Pirelli will collaborate in the related Research and Development

activities.

For Pirelli, the MOU also includes the possibility of entering into a long-term

supply agreement to purchase the synthetic rubber jointly produced by Rosneft

and the new technological partner being identified. SBR is of particular

interest as it is an eco-friendly material used in the production of “green

tyres”, which improves fuel efficiency and grip in both wet and dry conditions.

Marco Tronchetti Provera,

chairman and CEO of Pirelli, said: “The agreement signed today goes in the

direction of strengthening the synthetic rubber project in Nakhodka both

technologically and in terms of the already existing synergies between

Pirelli and Rosneft. It is also shows Pirelli and Rosneft beginning to

move together into new alliances which, as we

have already said, could also be a part of our future cooperation.”

Foundation Stone Laid at Ceremony to Mark

Launch of Construction of Eastern Petrochemical Company

A foundation stone laying ceremony has

been held at the construction site of the Eastern

Petrochemical Company outside Nakhodka. Construction work, which is

being carried out by Rosneft, was formally launched by Russian President

Vladimir Putin.

The petrochemical facility will produce

polypropene, high and low density polyethylene, monoethylene glycol and

other petrochemical products. Annually, it will process 3.4 mln

tonnes of feedstock supplied by Rosneft’s Achinsk and

Komsomolsk refineries and the Angarsk Petrochemical Company. Some of

the Eastern Petrochemical Company’s facilities will have higher capacity

than similar units elsewhere in the world. For instance, the

plant’s pyrolysis unit will produce 1.4 million tonnes

of ethylene a year. In terms of capacity, it will be unrivalled

globally.

Technologies for the plant will be

licensed from leading world-class specialist companies to ensure the

facility’s technical prowess and safety. Particular attention was paid to

environmental issues as early as at the design stage.

The complex is located close to

fast-growing South-East Asian markets and has its own sea terminal in an

ice-free port.

Construction of the facility will give a

strong boost to the regional economy with a multiplier effect increasing tax

returns at all levels. Thousands of new jobs will be created at the plant as

well as in related sectors with the region reaping corresponding social

benefits.

--------

24 May 2014

PIRELLI AND ROSNEFT FURTHER CONSOLIDATE RELATIONSHIP WITH TWO MOUs

On the industrial front, under the terms of the MOU, Pirelli will cooperate

jointly with Rosneft in activities to produce synthetic

rubbers in Nakhodka, including Styrene-Butadiene Rubber (SBR). Pirelli is

also interested in entering into a long-term supply agreement to purchase the

synthetic rubber produced. SBR is an eco-friendly material used in the

production of “green tyres” which improves fuel efficiency and grip in both wet

and dry conditions. This agreement follows an MOU signed for similar activities

in Armenia in December 2013.

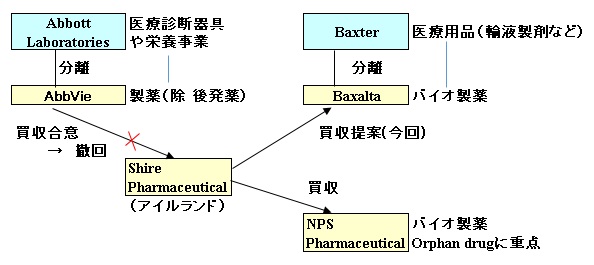

Mar 4, 2015 AbbVie

AbbVie to Acquire Pharmacyclics, including

its blockbuster product Imbruvica®, Creating an Industry Leading Hematological

Oncology Franchise

- Adds Imbruvica® a first in class BTK

inhibitor approved in multiple indications for blood cancers.

- Extensive clinical program with over 50

studies ongoing evaluating Imbruvica® as a treatment for a wide range of

additional indications, including early assessments for solid tumors and

potential treatment of Graft v Host disease.

- Broadens and deepens AbbVie's already

robust pipeline, and establishes the combined company as an emerging leader

in the hematological oncology space.

- Accelerates the company's commercial

presence in oncology.

- Transaction valued at $261.25 per

Pharmacyclics' share, total transaction value of approximately $21 billion

- Highly accretive to both revenue and

earnings by 2017.

AbbVie and Pharmacyclics today announced a

definitive agreement under which AbbVie will acquire Pharmacyclics, and its

flagship asset Imbruvica® (ibrutinib), a highly effective treatment for

hematologic malignancies. The acquisition accelerates AbbVie's clinical

and commercial presence in oncology, strengthening its already robust

pipeline, and establishing its strong leadership position in hematological

oncology – an attractive and rapidly growing market, now approaching

$24 billion globally. The

acquisition adds to AbbVie's already comprehensive pipeline and strong

growth prospects.

Under the

terms of the transaction, AbbVie will pay

$261.25 per share comprised of a mix of cash and AbbVie equity. The

transaction values Pharmacyclics at approximately

$21 billion and was approved

by the Boards of Directors of both companies.

Imbruvica® is a

Bruton's tyrosine kinase (BTK) inhibitor approved for use in four

indications to treat three different types of blood cancers including

chronic lymphocytic leukemia, mantle cell lymphoma and Waldenstrom's

macroglobulinemia. Imbruvica® received initial U.S. Food and Drug

Administration (FDA) approval in 2013 and is the only therapy to have

received three Breakthrough Therapy designations by the FDA. It is

currently approved in more than 40 countries. Significant opportunity

exists with further Imbruvica® indications, including solid tumors, the

potential to leverage AbbVie's immunology expertise for the development of

Pharmacyclics' immunology program, and advance AbbVie's efforts in

hematologic malignancies.

"The acquisition of Pharmacyclics is a

strategically compelling opportunity. The addition of Pharmacyclics'

talented and innovative team will add enormous value to AbbVie," said

Richard A. Gonzalez,

chairman and chief executive officer, AbbVie. "Its flagship product,

Imbruvica®, is not only complementary to AbbVie's oncology pipeline, it has

demonstrated strong clinical efficacy across a broad range of hematologic

malignancies and raised the standard of care for patients."

"Team Pharmacyclics is honored and

enthusiastic to join the AbbVie organization. We share a common purpose.

Together and as one, our focus remains to create a remarkable difference for

patient betterment around the world," said

Bob Duggan, chairman

and chief executive officer, Pharmacyclics.

Transaction Terms AbbVie will acquire all of the outstanding shares of common stock of

Pharmacyclics through a tender offer, followed by a second-step merger. In

the tender offer, AbbVie will offer to acquire all of the outstanding shares

of Pharmacyclics' common stock for $261.25

per share, consisting of cash and AbbVie common stock. Pharmacyclics'

stockholders will be permitted to elect cash, AbbVie common stock or a

combination, subject to proration. The aggregate consideration will consist

of approximately 58% cash and 42% AbbVie common stock. The closing of the

tender offer is subject to customary closing conditions, including

regulatory approvals, and the tender of a majority of outstanding shares of

Pharmacyclics' common stock, and is expected to close in mid-2015.

AbbVie will acquire all remaining shares

of Pharmacyclics' common stock that are not tendered in the tender offer

through a second-step merger, which will be completed immediately following

the tender offer and without a vote of Pharmacyclics' stockholders.

AbbVie expects to fund the transaction

through a combination of existing cash, new debt and stock.

About

Pharmacyclics Pharmacyclics, Inc. (NASDAQ: PCYC) is a biopharmaceutical company

focused on developing and commercializing innovative small-molecule drugs

for the treatment of cancer and immune mediated diseases. The company's

mission is to build a viable biopharmaceutical company that designs,

develops and commercializes novel therapies intended to improve quality of

life, increase duration of life and resolve serious unmet medical needs. It

will do so by identifying and controlling promising product candidates based

on scientific development and administrative expertise, developing its

products in a rapid, cost-efficient manner and, pursuing commercialization

and/or development partners when and where appropriate.

Pharmacyclics markets IMBRUVICA and has

three product candidates in clinical development and several preclinical

molecules in lead optimization. The company is committed to high standards

of ethics, scientific rigor and operational efficiency as it moves each of

these programs to commercialization. Pharmacyclics is headquartered in

Sunnyvale, CA. To learn more,

please visit

www.pharmacyclics.com.

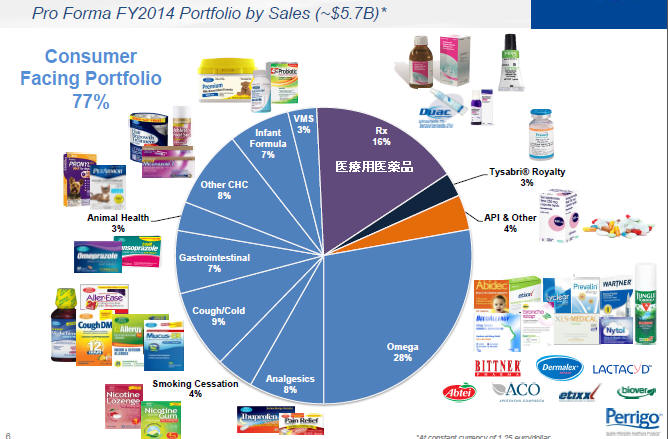

In 2013, Perrigo solidified its

global foothold by acquiring Elan Corporation plc

through formation of a new holding company, Perrigo Company plc,

now headquartered in Dublin, Ireland.

Mylan Proposes To Acquire Perrigo For $205 Per Share

Mylan N.V. today announced that Mylan has

made a proposal to acquire Perrigo Company plc in a cash-and-stock

transaction that would create a diversified, global pharmaceutical leader with

an unmatched commercial and operating platform and a unique, one-of-a-kind

profile. The combination of these highly complementary businesses would produce

a company with critical mass in specialty brands,

generics, over-the-counter (OTC) and nutritional products; a powerful

commercial platform with reach across all customer channels; an exceptional

high-quality operating platform; and opportunities to generate enhanced growth

and deliver significant immediate and long-term value and benefits for

shareholders and the other stakeholders of both companies.

Under the terms of the non-binding proposal, which was delivered to Perrigo's

Chairman on April 6, 2015, Perrigo shareholders would receive $205 in a

combination of cash and Mylan stock for each Perrigo share, which represents a

greater than 25% premium to the Perrigo trading

price as of the close of business on Friday, April 3, 2015 (the last trading

date prior to the date of Mylan's proposal), a greater than 29% premium to

Perrigo's sixty-day average share price and a greater than 28% premium to

Perrigo's ninety-day average share price.

Mylan's Executive Chairman Robert J. Coury commented, "This proposal is the

culmination of a number of prior discussions between Mylan and Perrigo about the

compelling strategic and financial logic of this combination. This combination

would result in meaningful immediate and long-term value creation, and our

proposal is designed to deliver that value to shareholders and other

stakeholders of both companies. We have great respect for Perrigo's board and

management team and what they have built. We look forward in the weeks ahead to

working with them to capitalize on this tremendous opportunity and working

together to create a unique leader with a one-of-a-kind profile in our

industry."

The proposal is subject to the pre-condition of confirmatory due diligence,

which pre-condition may be waived by Mylan at its discretion. This announcement

is not an announcement of a firm intention to make an offer under rule 2.5 of

the Irish Takeover Panel Act, 1997, Takeover Rules 2013 and there can be no

certainty that an offer will be made, even if the due diligence pre-condition is

satisfied or waived. A further statement will be made if and when appropriate.

ーーーーー

About Perrigo

Perrigo Company plc, a top five global

over-the-counter (OTC) consumer goods and pharmaceutical company, offers

consumers and customers high quality products at affordable prices. From its

beginnings in 1887 as a packager of generic home remedies, Perrigo,

headquartered in Ireland, has grown to become

the world's largest manufacturer of OTC products and supplier of infant formulas

for the store brand market. The Company is also a leading provider of

generic extended topical prescription products and

receives royalties from Multiple Sclerosis drug Tysabri®. Perrigo provides "Quality

Affordable Healthcare Products®" across a wide variety of product

categories and geographies primarily in North America,

Europe, and Australia,

as well as other key markets including Israel

and China.

Perrigo develops, manufactures and

distributes over-the-counter (OTC) and generic prescription (Rx)

pharmaceuticals, nutritional products and active pharmaceutical ingredients

(API), and receives royalties from Multiple Sclerosis 多発性硬化症drug Tysabri®.

Perrigo Consumer Healthcare (CHC) markets a

broad line of over-the-counter (OTC), diabetes and animal

healthcare products that are comparable in quality and effectiveness to

the advertised brands. Perrigo CHC supplies more than 500 formulas in nearly

every major OTC category: analgesics, pediatric analgesics, cough and cold,

gastrointestinal, nicotine replacement, allergy, feminine hygiene, as well as

blood glucose meters, test strips and supplies for the diabetes market. Perrigo

CHC also markets several animal healthcare products, pet treats and

miscellaneous pet care items. Perrigo is the store brand leader in creating

comprehensive marketing programs and campaigns that support all OTC categories –

in-store, e-commerce and digital media.

Perrigo is one of the United States' largest

manufacturers of nutrition products for the store brand market. Nutrition

products include infant formula, pediatric

nutritionals and vitamins, minerals, and supplements.

Perrigo API (formerly known as Chemagis)

provides differentiated Active Pharmaceutical Ingredients (APIs) and Finished

Dosage Forms (FDFs) for the branded and generic pharmaceutical industries.

TYSABRI® is marketed and distributed solely

by Biogen. Perrigo receives royalties on in-market sales.

May 6, 2015

Alexion to Acquire Synageva to

Strengthen Global Leadership in Developing and Commercializing

Transformative Therapies for Patients with Devastating and Rare Diseases

-- Expands

Alexion’s metabolic franchise with the addition

of Kanuma™ (sebelipase alfa) for LAL Deficiency

(LAL-D) --

-- Launches of Kanuma and

Alexion’s Strensiq™ (asfotase

alfa) expected in 2015 --

-- Creates the most robust rare disease pipeline

in biotech; adds SBC-103 for MPS IIIB to

clinical development programs --

-- Combined pipeline to have eight highly

innovative product candidates in the clinic for

eleven indications --

-- Preclinical pipeline to have more than 30

diverse programs across a range of therapeutic

modalities, including 12 from Synageva’s novel

drug discovery platform, with at least four

additional programs to enter the clinic in 2016

--

-- Transaction valued at $8.4 billion net of

cash --

-- Accelerates and diversifies Alexion’s growing

revenues starting in 2015 --

-- Accretive to non-GAAP EPS in 2018 --

-- Alexion Board increases authorized share

repurchase to a total of $1 billion --

Alexion Pharmaceuticals,

Inc. and Synageva BioPharma Corp. announced today that they

have entered into a definitive agreement pursuant to which

Alexion will acquire Synageva for consideration of $115 in

cash and 0.6581 Alexion shares, for each share of Synageva,

implying a total per share value of $230 based on the nine

day volume-weighted average closing price of Alexion stock

through May 5, 2015. The acquisition strengthens Alexion’s

global leadership in developing and commercializing

transformative therapies for patients with devastating and

rare diseases.

The transaction has been

unanimously approved by both companies’ Boards of Directors,

and is valued at approximately $8.4

billion net of Synageva’s cash. The transaction is

expected to accelerate and diversify Alexion’s growing

revenues, and Alexion expects to achieve annual cost

synergies starting this year and growing to at least $150

million in 2017. In addition, the transaction is expected to